(+91) 9445444862

(+91) 9445444862 Info@indbiz.in

Info@indbiz.in

Learn how to get a credit card with no credit history in India. Step-by-step guide, best beginner cards, tips to build your CIBIL score fast.

How to Get a Credit Card with No Credit History in India

Introduction

Imagine this situation.

You apply for your first credit card, expecting approval within minutes. But instead, the bank rejects your application.

The reason?

“No credit history.”

This is one of the most common financial problems for young professionals, students, and first-time earners in India.

Banks want to see a credit history before giving a credit card, but you need a credit card to build a credit history. This creates a frustrating loop for many beginners.

The good news is that getting a credit card without a credit history is absolutely possible — if you know the right strategies.

In this guide, you will learn:

- How credit history works

- Why banks reject first-time applicants

- Practical ways to get your first credit card

- Smart tips to build your credit score quickly

By the end of this article, you will know exactly how to get approved for your first credit card in India.

Table of Contents

- What Is Credit History?

- Why Banks Reject Applicants with No Credit History

- Ways to Get a Credit Card Without Credit History

- Best Beginner Credit Cards in India

- Secured Credit Cards Explained

- How to Build Your Credit Score Quickly

- Real-Life Example: First Credit Card Strategy

- Common Mistakes to Avoid

- Frequently Asked Questions

- Conclusion

What Is Credit History?

Your credit history is a record of how you manage borrowed money.

Banks track your financial behavior through credit bureaus such as CIBIL, Experian, and Equifax.

Your credit report includes:

- Loans taken

- Credit cards used

- Payment history

- Credit limits

- Outstanding balances

From this information, a credit score is calculated.

CIBIL Score Range

| Score Range | Meaning |

|---|---|

| 750 – 900 | Excellent |

| 700 – 749 | Good |

| 650 – 699 | Average |

| 550 – 649 | Risky |

| Below 550 | Poor |

If you never borrowed money before, your credit report shows:

“No credit history.”

This makes banks cautious because they cannot evaluate your repayment behavior.

Why Banks Reject Applicants with No Credit History

Banks use credit scores to predict risk.

If there is no financial track record, banks cannot determine:

- Whether you pay bills on time

- Whether you manage credit responsibly

- Whether you are likely to default

From a lender’s perspective, approving a card for someone without credit history is uncertain.

Common applicants with no credit history include:

- Students

- Fresh graduates

- First job professionals

- Self-employed beginners

- People who only use debit cards

Fortunately, there are several ways to bypass this problem.

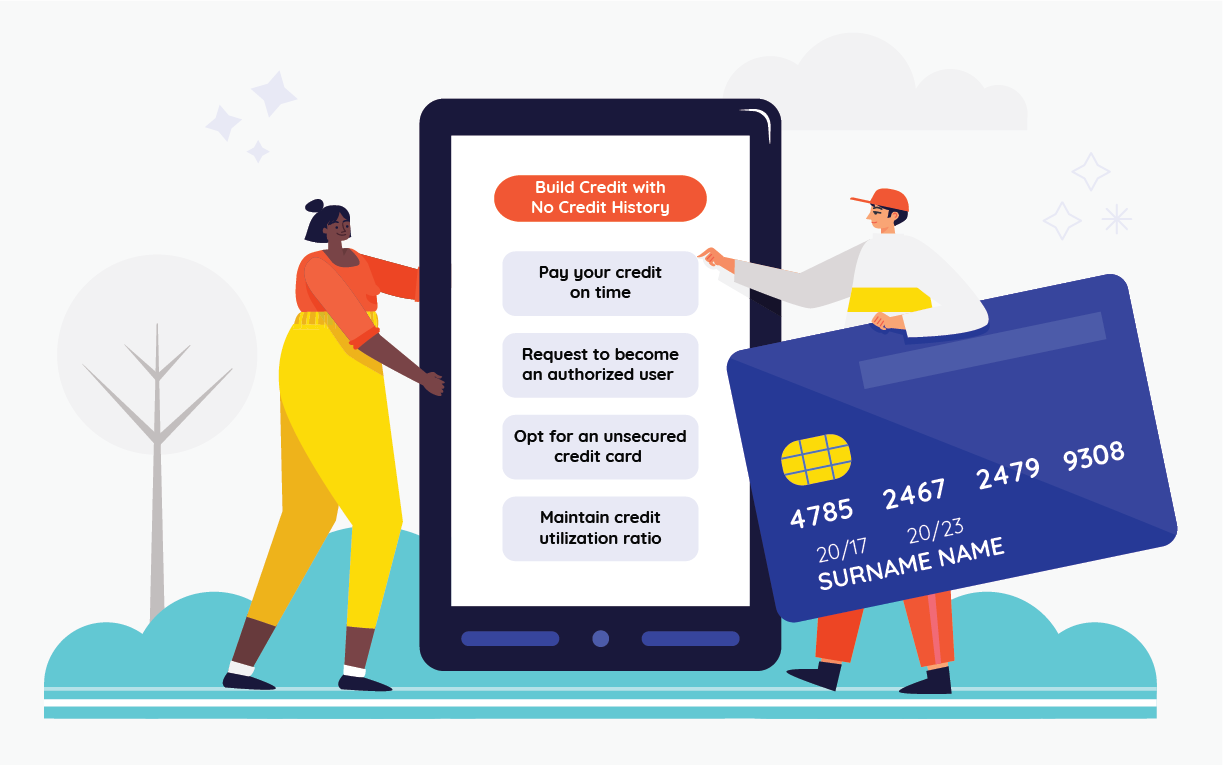

Ways to Get a Credit Card Without Credit History

1. Apply for a Secured Credit Card

This is the easiest way to get your first credit card.

A secured credit card is issued against a fixed deposit (FD).

Example:

- Fixed deposit: ₹20,000

- Credit card limit: ₹15,000–₹18,000

Because the bank holds your deposit as collateral, approval becomes easy.

Benefits

- Almost guaranteed approval

- Builds credit history

- Helps increase CIBIL score

- Converts to normal card later

Many banks in India offer secured credit cards.

2. Apply Through Your Salary Account Bank

If you have a salary account, your bank already knows your income.

This increases your chances of approval.

Banks often provide pre-approved credit cards to salary account holders.

Advantages:

- Higher approval probability

- Faster processing

- Better credit limits

3. Apply for Entry-Level Credit Cards

Some credit cards are specifically designed for beginners.

These cards usually have:

- Lower credit limits

- Basic rewards

- Easy eligibility

They help people build credit history safely.

4. Get an Add-On Credit Card

An add-on card is linked to someone else’s primary credit card.

Example:

- Parent has a credit card

- You receive an add-on card under their account

Benefits:

- Helps build credit history

- No income requirement

- Easy approval

However, spending responsibility remains important.

5. Use Buy Now Pay Later (BNPL) Services

BNPL platforms like:

- Amazon Pay Later

- Flipkart Pay Later

- LazyPay

- Simpl

Some of these services report to credit bureaus, helping you build a credit profile.

However, use them carefully and pay on time.

Best Beginner Credit Cards in India

Here are some popular credit cards suitable for first-time users.

| Credit Card | Best For | Annual Fee |

|---|---|---|

| HDFC MoneyBack Card | Cashback rewards | ₹500 |

| SBI SimplySAVE Card | Shopping rewards | ₹499 |

| ICICI Platinum Chip Card | Beginners | Free |

| Axis Bank Insta Easy Card | Secured card | FD based |

| IDFC FIRST Millennia Card | Rewards | Free |

These cards offer simple rewards and easy approval conditions.

Secured Credit Cards Explained

A secured credit card works like a normal credit card, but it is backed by your deposit.

Example Scenario

Rahul opens a ₹25,000 fixed deposit.

The bank gives him:

- Credit limit: ₹20,000

- Credit card approval: Instant

Rahul uses the card responsibly for 6–12 months.

His CIBIL score increases.

Later, the bank upgrades him to a regular credit card.

This is one of the fastest ways to start building credit history.

How to Build Your Credit Score Quickly

Once you get your first credit card, your next goal is to build a strong credit score.

Follow these best practices.

1. Pay Bills on Time

Payment history contributes to 35% of your credit score.

Even one late payment can reduce your score.

Tip:

Set auto-pay for credit card bills.

2. Keep Credit Utilization Low

Credit utilization means how much of your limit you use.

Example:

| Credit Limit | Spending | Utilization |

|---|---|---|

| ₹50,000 | ₹10,000 | 20% |

| ₹50,000 | ₹40,000 | 80% |

Experts recommend keeping utilization below 30%.

3. Avoid Multiple Applications

Applying for many credit cards quickly can hurt your score.

Every application creates a hard inquiry on your credit report.

Too many inquiries signal credit risk.

4. Maintain Old Accounts

The length of credit history improves your score.

Keep your first credit card active even if you upgrade later.

5. Use Credit Regularly but Responsibly

Small monthly expenses such as:

- Fuel

- Groceries

- Utility bills

Using your credit card for these and paying on time helps build a healthy credit profile.

Real-Life Example: First Credit Card Strategy

Let’s look at a practical example.

Situation

Anita, age 24, just started her first job.

She has:

- No loans

- No credit history

- No CIBIL score

Step 1

She opens a ₹30,000 fixed deposit.

Step 2

The bank issues a secured credit card with ₹25,000 limit.

Step 3

She uses the card for:

- Groceries

- Mobile bill

- Fuel

Total monthly spending: ₹8,000.

Step 4

She pays the bill in full every month.

Result after 6 months:

Her CIBIL score increases to around 740+.

Now she becomes eligible for premium credit cards.

Common Mistakes to Avoid

Many beginners damage their credit score unintentionally.

Avoid these mistakes.

1. Missing Payments

Late payments can reduce your score significantly.

Always pay before the due date.

2. Maxing Out the Card

Using 90–100% of your credit limit signals financial stress.

Keep usage below 30–40%.

3. Cash Withdrawals

Credit card cash withdrawals have:

- High interest

- Extra fees

Avoid using your card for ATM withdrawals.

4. Applying for Too Many Cards

Multiple applications can trigger credit rejection patterns.

Apply strategically.

Frequently Asked Questions

1. Can I get a credit card without a CIBIL score?

Yes. Secured credit cards or entry-level cards allow approval even without a credit score.

2. What is the easiest credit card to get in India?

Secured credit cards issued against fixed deposits are the easiest to obtain.

3. How long does it take to build a credit score?

Usually 3 to 6 months of responsible credit card usage can generate your first credit score.

4. What is the minimum CIBIL score for credit cards?

Most banks prefer a score above 700, but beginner cards may accept lower scores.

5. Can students get credit cards in India?

Yes. Students can obtain secured credit cards or add-on cards from parents.

6. Does debit card usage build credit score?

No. Debit cards do not report activity to credit bureaus.

Only credit products affect your credit score.

7. What happens if I don’t use my credit card?

Inactive cards may be closed by banks, which can reduce your credit history length.

Use your card occasionally.

8. Is it safe to use credit cards?

Yes, if used responsibly. Paying the full balance every month avoids interest charges.

Conclusion

Getting your first credit card without a credit history may seem difficult, but it is completely achievable with the right approach.

The most reliable methods include:

- Applying for a secured credit card

- Using your salary account bank

- Starting with entry-level credit cards

- Building credit through small, responsible usage

Remember, a credit card is not just a spending tool — it is also a financial reputation builder.

If you use it wisely, you can quickly build a strong CIBIL score, which helps you qualify for:

- Personal loans

- Home loans

- Premium credit cards

- Lower interest rates

Your first credit card is the foundation of your financial future.

Use it carefully, pay on time, and your credit profile will grow stronger every year.

Disclaimer:

This article is for educational purposes and should not be considered financial advice.